Think back to what school prepared you for. You can probably still rattle off the quadratic formula or name the parts of a cell. But the first time you stared at a pay stub wondering where half your money went, or tried to make sense of a W-2, a credit card APR, or a lease — odds are nobody had ever walked you through it. Most of us figured out money the hard way, leaning on a parent, a friend, or plain trial and error.

Some kids have those guides at home. Many don’t. And the gap between the two shows up later in life with real consequences.

The Numbers Aren’t Subtle

Financial literacy in the U.S. has been stuck at low levels for a decade. On the most recent Personal Finance Index, adults answered fewer than half of basic money questions correctly — a figure that has never topped 52% in ten years of tracking.¹ The youngest adults score worst of all, with Gen Z averaging about 38%.¹

That knowledge gap is expensive. Adults with very low financial literacy are roughly three times as likely to be financially fragile — unable to absorb a surprise expense — and about twice as likely to be constrained by debt.² When you don’t understand how interest, credit, and saving work, small money decisions quietly compound in the wrong direction.

Here’s the kicker: most people never learned this in a classroom at all. In one national survey, only 15% of adults said school was where they learned the most about money, while 38% pointed to family.³ And the majority say their own high school didn’t even offer a personal finance class.⁴

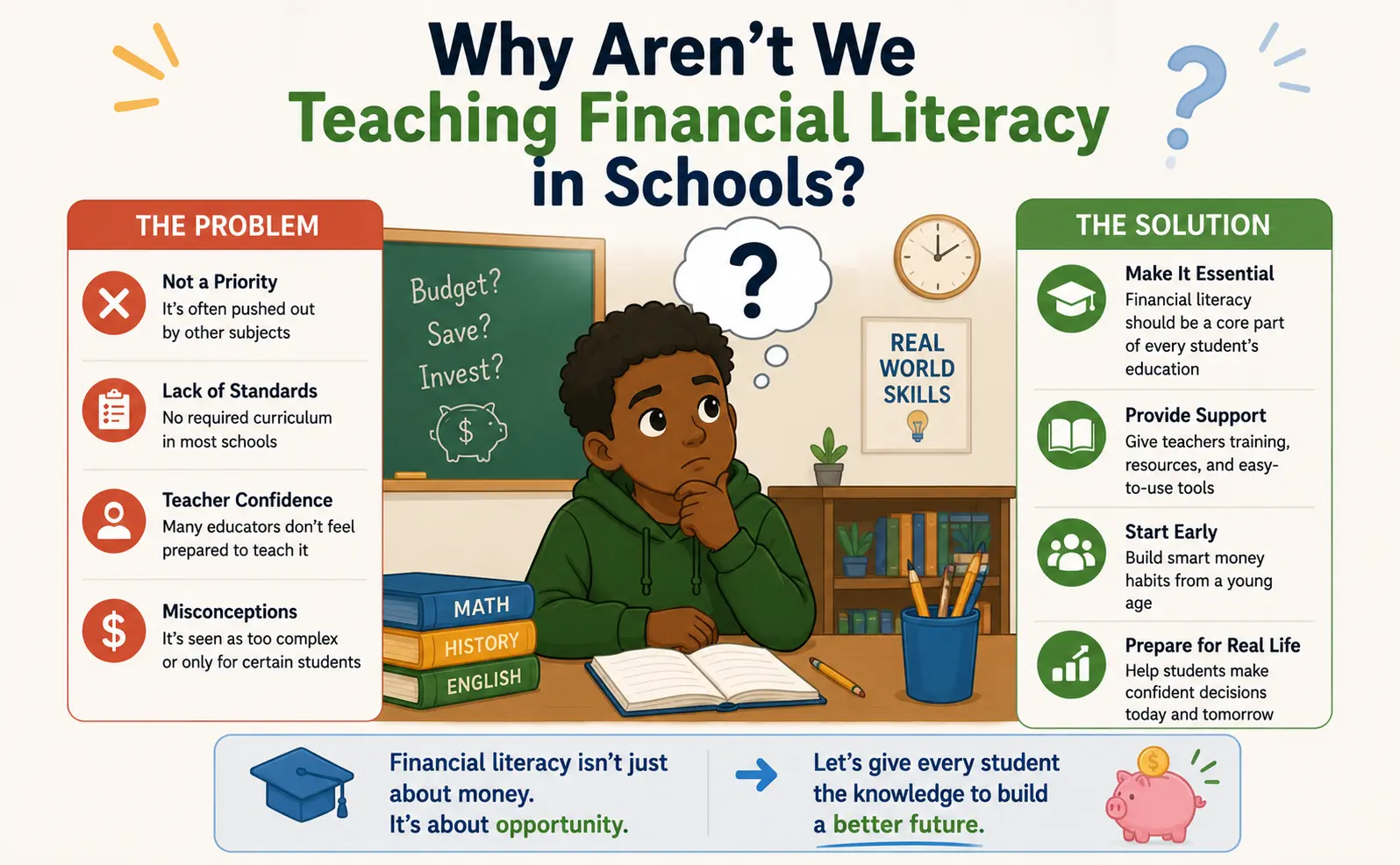

So Why Isn’t It a Priority?

It’s not for lack of wanting it. Support for teaching personal finance is overwhelming and rare in how bipartisan it is — in recent polling, more than 80% of adults said they wish they’d been required to take a personal finance course in high school, and agreement that it should be taught crosses party lines almost evenly.⁵ Parents want it. Students want it. Teachers want it.

The obstacle is the school day itself. Between packed curricula, high-stakes testing, and limited time and training, financial literacy keeps getting squeezed out — and many teachers who do teach it end up seeking the training on their own.⁶ Even where a personal finance course exists, it usually arrives in high school, long after kids have started forming money habits. Research suggests those habits begin taking shape remarkably early — a widely cited University of Cambridge study found that many are largely set by around age seven.⁷ By the time a formal course shows up, students have already missed years of habit-building, and the kids with the least support at home are often the ones with the least access to it at school.

The good news is that the picture is improving fast: as of late 2025, 30 states guarantee every high schooler a standalone personal finance course, and by 2031 the majority of U.S. graduates will have taken one.⁸ But more than a quarter of students still live in a state without that guarantee — and a once-a-semester high school course can’t, by itself, undo years of missed practice.⁸

What Actually Works: Practice, Not Lectures

Here’s the part the research keeps returning to: financial literacy sticks when students do it, not just hear about it. A worksheet on compound interest is forgettable. Watching your own savings balance tick upward, week after week, is not.

That’s the whole idea behind a classroom economy. Give every student an account, pay them for classroom jobs, charge them rent, open a class store, and suddenly money stops being abstract. Kids practice earning, budgeting, saving toward a goal, and living with the consequences of their choices — in a setting where the stakes are pretend but the lessons are real. It folds financial literacy into the daily rhythm of the classroom instead of carving out a separate unit nobody has time for.

The catch has always been the workload. Running a paper-based economy — minting fake bills, tracking balances by hand, distributing currency for a roomful of students — is the kind of thing teachers abandon by October. The tracking eats the time the lesson was supposed to save.

That’s Why We Built Fun Banking

Fun Banking takes everything good about a classroom economy and removes the paperwork. Students log in with a secure PIN and manage their own checking and savings accounts. You set up automated payroll and recurring bills, run a school store with digital receipts, and approve transactions from one dashboard. From there, students can explore the concepts that actually shape adult financial life — saving versus spending, transferring between accounts, even credit cards, loans, and certificates of deposit — all in a safe simulation with no real money involved.

Whether you want a simple setup to get started this week or the full toolkit to build a rich, multi-account economy, it’s designed to slot into your classroom without adding to your plate. Because the goal isn’t more work for teachers. It’s making sure every student — not just the ones with a money mentor at home — gets to practice the skills that follow them for life.

👉 Start free with Fun Banking · See all features · Compare plans